Corporate Governance UPSC

Corporate governance refers to the set of regulations, methods, and legal frameworks that guide the functioning, oversight, and management of businesses. It encompasses a wide range of factors that influence the concerns and well-being of a company’s stakeholders. These stakeholders include shareholders, customers, suppliers, government authorities, and the management team.

Sir Adrian Cadbury who is known as father of corporate governance defines it as ‘the way company is controlled & directed’.

Implication of this meaning is that the manner of controlling & directing should be based on set of standards i.e. companies should be run on basis of set of standards so that there are transparency, accountability & protection of all share holders & stake holders including citizen.

“You can fool some of the people all of the time, and all of the people some of the time, but you can not fool all of the people all of the time.”

Abraham Lincoln

“Corporate governance should go the realm of law, it should emanate from management culture.” –

Narayan Murthy

Need for Corporate Governance

1. Corporate failures (PNB scam, Satyam, Sharada scams)

2. Corporate coup (Tata company)

3. Corporate corruption (Nirav Modi, Vijay Mallya)

4. Promoting competition, quality, cost effectiveness, entrepreneurship, innovation, creativity.

5. Protecting interest of citizen, society.

Importance of Corporate Governance

Corporate governance is established upon a framework of regulations, internal rules, policies, and processes designed to ensure transparency and accountability within a company. When implemented effectively, it creates a structure that guides the achievement of a company’s goals across all aspects of management. It also acknowledges the significance of shareholders.

Shareholders actively engage in the company’s decision-making by selecting board members, contributing to financial operations, and influencing the company’s functioning.

Sound governance safeguards a company’s ethics, overall direction, risk management, and strategic planning. This, in turn, enables companies to remain financially strong and foster robust relationships with their communities, shareholders, and investors, fostering trust. Demonstrating strong corporate governance is often seen as just as crucial as achieving profitability for businesses.

Conversely, inadequate corporate governance can result in various negative consequences, including: inability to attain company objectives; erosion of support from stakeholders and communities; financial setbacks; and potential collapse of the business.

Essentially, corporate governance is the way a company regulates itself. It’s akin to running a business as if it were a self-governing nation, enforcing the company’s own standards, policies, and regulations across all levels of the organization.

Four segment of Corporate governance

Equity:

The board of directors holds the duty to treat shareholders, employees, suppliers, and communities justly and equitably, giving each group equal consideration.

Openness:

The board is tasked with furnishing timely, precise, and transparent information regarding aspects like financial performance, conflicts of interest, and potential risks to both shareholders and other stakeholders.

Risk Oversight:

Both the board and management are required to identify various risks and devise effective strategies to manage them. They should then put these strategies into action and communicate the presence and status of risks to all relevant parties.

Oversight:

The board bears the responsibility of supervising corporate affairs and managerial operations.

It should be well-informed about and supportive of the company’s ongoing success and performance. Additionally, it’s responsible for selecting and appointing a CEO. Acting in the best interests of the company and its investors is a key aspect of this responsibility.

Answerability:

The board is obligated to clarify the purpose behind the company’s actions and the outcomes of its conduct. Both the board and company leadership are held accountable for evaluating the company’s capabilities, potential, and achievements. Furthermore, they must relay significant matters to shareholders in a clear and concise manner.

Aim of Corporate Governance

The central aim of corporate governance is to enhance both the operational efficiency and responsibility of a company, with the ultimate objective of augmenting the value for shareholders and safeguarding the concerns of various stakeholders.

In essence, it seeks to establish a harmonious equilibrium within a company, ensuring that while the pursuit of enhanced shareholder wealth remains a priority, it is done so in a manner that doesn’t compromise the legitimate interests of other stakeholders associated with the company.

Additionally, corporate governance seeks to cultivate an environment of credibility and trust among those individuals and entities that possess divergent and potentially conflicting interests.

This factor is pivotal for a company’s sustained existence, as it instills a sense of assurance and conviction in investors by showcasing the company’s unwavering dedication to fostering growth and augmenting profits in a responsible and ethical manner.

Here are two example of Conflict of Interest and Corporate governance.

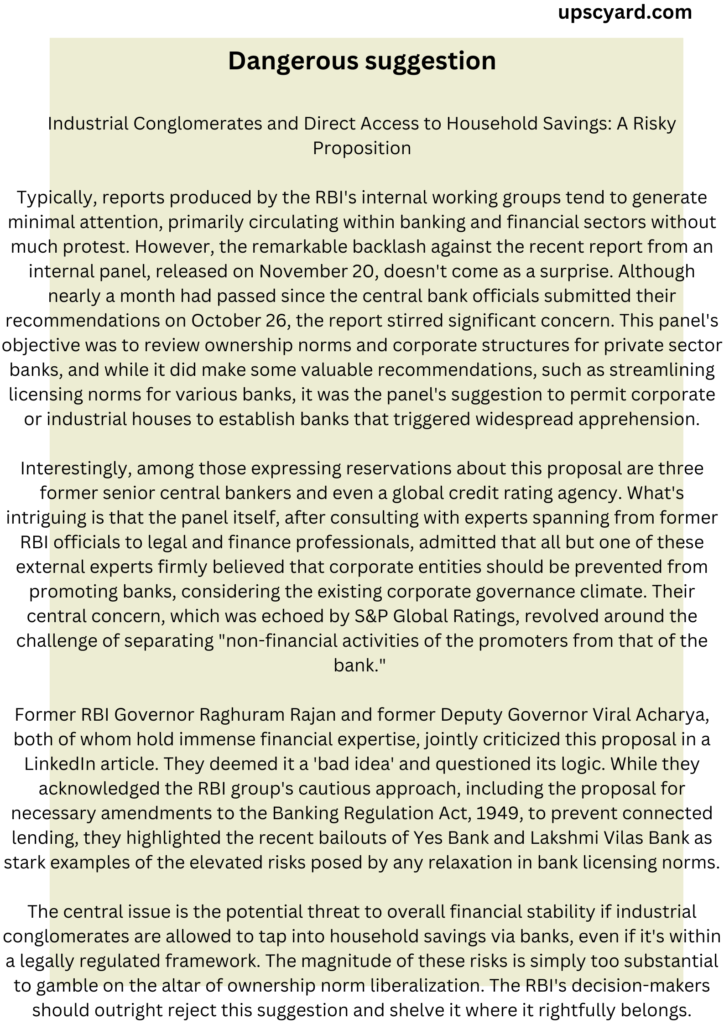

1.Why it’s Inadvisable for Business Tycoons to Manage Banks

2.

Corporate Governance UPSC initiatives in Indian context

In India, the Ministry of Corporate Affairs (MCA) and the Securities and Exchange Board of India (SEBI) have spearheaded corporate governance initiatives. The formal regulatory framework for corporate governance aimed at listed companies was introduced by SEBI in February 2000, following the guidance of the Kumarmangalam Birla Committee Report. This framework, known as Clause 49 of the Listing Agreement, set the initial standards.

SEBI continues to uphold corporate governance standards through other legislations such as the Securities Contracts (Regulation) Act, 1956; Securities and Exchange Board of India Act, 1992; and Depositories Act, 1996.

In 2002, the Ministry of Corporate Affairs established the Naresh Chandra Committee on Corporate Audit and Governance to address corporate governance concerns comprehensively. The committee’s recommendations covered vital aspects like financial and non-financial disclosures, independent auditing, and board supervision of management.

The enactment of the Companies Act 2013 and its amendments reflects the ministry’s dedication to enhancing transparency within corporate governance structures.

India’s SEBI Committee on Corporate Governance defines corporate governance as “management’s recognition of shareholders’ inherent rights as the true proprietors of the corporation, and of their own role as guardians on behalf of the shareholders. It encompasses commitment to principles, ethical business conduct, and the differentiation between personal and corporate finances in company management.”

While the Indian approach resonates with the Gandhian principle of trusteeship and the Directive Principles of the Indian Constitution, this perception of corporate objectives is also prevalent in Anglo-American and numerous other legal jurisdictions.

To foster improved corporate governance practices in India, the Ministry of Corporate Affairs, in collaboration with the Confederation of Indian Industry (CII), Institute of Company Secretaries of India (ICSI), and Institute of Chartered Accountants of India (ICAI), has founded the National Foundation for Corporate Governance (NFCG). This initiative is geared towards advancing the realm of corporate governance in the country.

Corporate Governance failures – examples

- Satyam

- IL & FS

- Yes Bank

- Dewan Housing

- Ranbaxy

UPSC CSE Previous year questions

Q. What do you understand by the terms ‘governance’, ‘good governance’ and ‘ethical governance’? (2016)

Q. In the light of the Satyam Scandal (2009), discuss the changes brought in corporate governance to ensure transparency and accountability. (2015)